This cost remains fixed over certain period of time irrespective of units produced. For example rent of building .It’s important to note that fixed cost remains fixed for certain level of activity , after which it increases

Although total cost is fixed for a period but as the number of units increases, the fixed cost per unit decreases.

Fixed cost

100,000

100,000

Number of units produced

100

200

Cost per unit

100,000/100 = 1000

100,000/200 = 500

FIXED COST

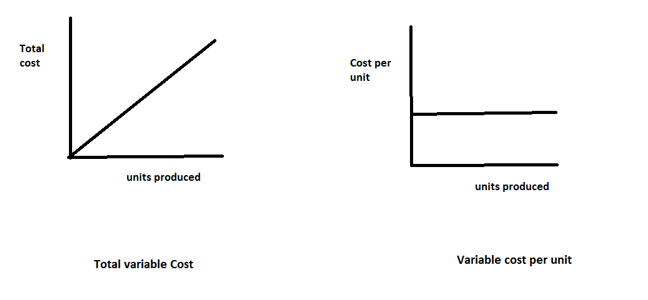

Variable Cost

Cost that increases with number of units produced. E,g material cost per unit. Total of variable costs increases per but per unit variable cost remain same

Variable cost

100,000

120,000

Number of units produced

100

200

Cost per unit

100,000/100 = 1000

120,000/200 = 1000

Variable Cost

Semi Variable Cost:

Cost that is partly fixed and partly variable .Such type of costs contain both fixed and variable portions.

Examples

Telephone bill

Electricity bill

Suppose According to electricity bill rules ,gave following rates are applicable:

Fixed cost up to 300 units =$ 3000

Units higher than 300 = 20$ per unit

If company ABC uses 500 units then

For first 300 units = 3000

For next 200 units = 200* 20 = 4000

Total cost = $ 7000

Semi Variable Cost

Stepped Costs:

Cost that is fixed for certain limit, but after that limit it increases. For example fix rent of building is $10,000 with capacity to produce 100,000 units. If production exceeds 100,000 units company have to take some other building on rent, which will increase fixed cost of $10,000. Let’s say other rent of other building taken on rent is again 100,000 with capacity to produce another 10,000 units, so cost will again remain fix till 20,000 units and will step up ,if production increases more than 20,000 units