A Comprehensive Guide to the Law of Supply and Supply Curve

Introduction:

The concept of supply is a fundamental aspect of economic theory, playing a crucial role in determining market equilibrium, influencing prices, and shaping production decisions. In this article, we will delve into the intricacies of supply, exploring the law of supply, the supply curve, and the various factors that influence them. By the end of this article, you should have a comprehensive understanding of supply and its impact on market dynamics.

The Law of Supply:

Definition and Explanation:

The law of supply is a fundamental principle in economics that states that, all other factors being constant (ceteris paribus), the quantity supplied of a good or service is directly proportional to its price. In simpler terms, as the price of a product increases, producers are willing and motivated to supply more of it, and as the price decreases, producers tend to supply less. This direct relationship between price and quantity supplied reflects producers’ rational decision-making based on profit maximization.

Factors Influencing Supply:

Price is the primary factor influencing supply, but several other variables also come into play. These include the cost of production, technology and innovation, expectations, the number of suppliers, and government policies. Understanding these factors is essential for predicting how market conditions and external influences can impact the supply of a product.

Cost of Production:

The cost of production includes factors such as raw materials, labor, overhead expenses, and taxes. As production costs increase, suppliers may be reluctant to supply the same quantity at a given price, leading to a decrease in supply. Conversely, technological advancements or efficiency improvements that lower production costs can result in an increase in supply.

Technology and Innovation:

Advancements in technology and innovation can significantly impact supply. New technologies can enhance production processes, increase efficiency, and reduce costs, leading to an increase in supply. For example, the introduction of automation in manufacturing can boost production capacity and supply.

Expectations:

Suppliers’ expectations about future market conditions, demand, and price movements can influence their current production and supply decisions. If suppliers anticipate higher prices or increased demand in the future, they may be incentivized to increase supply in the present.

Number of Suppliers:

The presence of more suppliers in a market can lead to an increase in overall supply. Greater competition among suppliers may drive them to expand production and capture a larger market share. Conversely, a decrease in the number of suppliers can result in a reduction in supply.

Government Policies:

Government interventions, such as taxes, subsidies, regulations, and trade policies, can significantly impact supply. For example, subsidies for certain industries or products can encourage increased supply, while taxes or regulatory restrictions may discourage supply.

The Supply Curve:

Definition and Explanation:

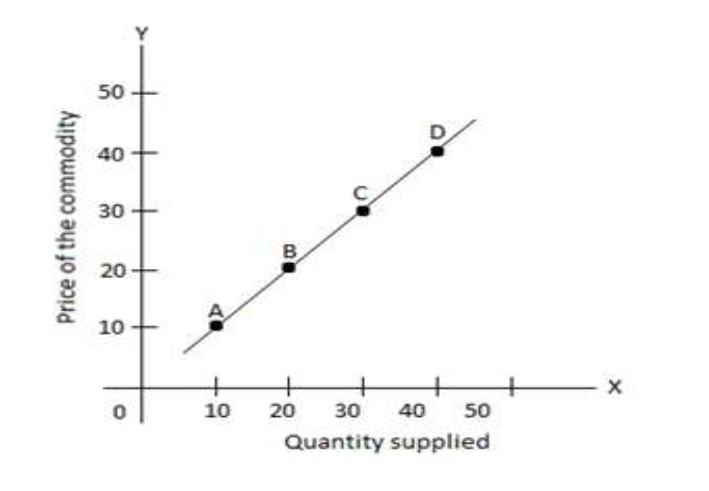

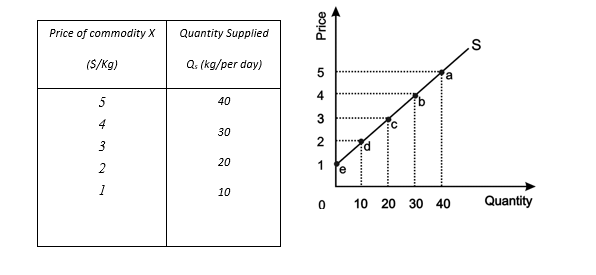

The supply curve is a graphical representation of the relationship between the price of a good or service and the quantity supplied. It is typically depicted as an upward-sloping line, with price on the vertical axis and quantity supplied on the horizontal axis. This curve illustrates the law of supply by showing that as price increases, the quantity supplied also increases, and vice versa.

Shape of the Supply Curve:

The shape of the supply curve can vary depending on factors such as the availability of resources, technology, and the number of suppliers. In most cases, the supply curve exhibits a positive slope, indicating that producers are willing to supply more at higher prices. However, in certain situations, such as with natural monopolies or resource constraints, the supply curve may be relatively inelastic, resulting in a flatter slope.

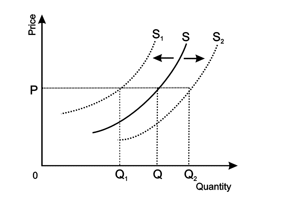

Factors Shifting the Supply Curve:

Changes in factors other than price, such as production costs, technology, or government policies, can lead to shifts in the supply curve. These shifts represent changes in the overall supply at each price level, causing the entire curve to move either to the right (increase in supply) or to the left (decrease in supply).

Real-World Examples:

Price Change:

Consider the market for crude oil. When the price of crude oil increases, oil-producing companies are incentivized to extract and supply more oil, leading to an increase in the quantity supplied. Conversely, a decrease in oil prices may result in reduced production and supply.

Cost of Production:

Imagine a scenario where technological advancements significantly reduce the cost of manufacturing solar panels. This decrease in production cost is likely to encourage more companies to enter the solar panel market, leading to an increase in supply.

Government Policies:

The introduction of subsidies for renewable energy sources can positively impact supply. For instance, government subsidies for wind farm operators may encourage more investment in wind energy production, resulting in an increase in the supply of renewable electricity.

Number of Suppliers:

In the market for smartphones, the presence of multiple competing manufacturers leads to an overall increase in supply. The intense competition among suppliers drives them to continuously innovate, expand production capacity, and capture market share.

Expectations:

Suppliers’ expectations about future market conditions can influence their production decisions. For example, if suppliers anticipate a surge in demand for electric vehicles in the coming years, they may start ramping up production and supply of electric car batteries in the present.

Conclusion:

Understanding supply is essential for comprehending market dynamics and economic behavior. The law of supply highlights the direct relationship between price and quantity supplied, while the supply curve visually represents this relationship. Various factors, such as production costs, technology, government policies, and expectations, influence supply and can lead to shifts in the supply curve. By analyzing real-world examples, we can grasp how changes in these factors impact supply, ultimately shaping market equilibrium and prices.

SUPPLY

Means the quantity of a product which the suppliers produce and brought for sale in the market

The law of supply:

Other factors remain constant, when prices of a product increases its supply also increases and vice versa

Thus the quantity supplied varies directly with price.

Supply schedule & curve:

Rise/Fall in Supply Curve

The price of the good causes change along supply line, while the other factors shift in supply curve. When supply increases, it shifts to the right and when decreases it shifts to the left.